July 10, 2023

Earlier this month, the U.S. government released multiple reports projecting how the U.S. grid electricity supply may shift over the next 7 years with consideration of how the Inflation Reduction Act (IRA) and the Infrastructure Investment and Jobs Act (IIJA) will impact the energy sector. For many businesses, the implications of these acts make decisions on energy transition timing critical as the calculus for investing in bridge fuels has changed significantly.

The third week of March marked three major energy reports from multiple agencies:

- Energy Information Administration’s Annual Energy Outlook 2023

- National Renewable Energy Laboratory’s analysis of the IRA and the IIJA

- Department of Energy Office of Policy’s Power-Sector Transitions projection

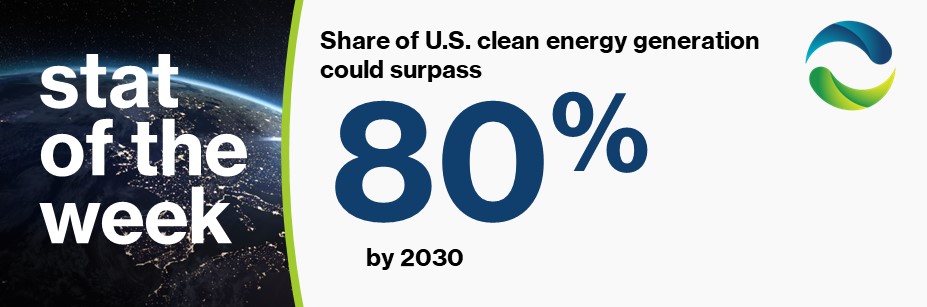

We now have multiple scenarios estimating changes to the U.S. energy sector through 2030. The big picture? Renewable energy deployment is projected to get a massive boost, propelling the U.S. grid to reach 71-90% of energy produced from clean sources by 2030, up from 41% in 2022. Prior to the passage of Inflation Reduction Act, clean energy generation was projected to reach~52% by 2030. This larger portion of clean energy generation would lead to CO2 emissions reductions of 26-38% for all U.S. energy-related emissions, or 72-91% below a 2005 baseline for the power sector. In addition to lower emissions, the increased supply of solar, wind, and other clean energy is projected to lead to 5-13% lower bulk energy costs than would otherwise be the case—that’s 3-6 USD/MWh.

However, the lower bulk energy costs of this transition do not capture other fees or transmission and distribution costs, so it’s unlikely energy consumers will reap the full savings. The cost of addressing transmission and distribution infrastructure is one of the most recognized obstacles to maximal adoption of renewable energy. Significant upgrades to the grid are necessary to ensure the U.S. energy system deploys renewable energy close to the higher end of these projections. Monitoring the pace and approach utilities, grid operators and legislatures take in response to this challenge will be key for corporate executives in the years ahead.

While no model is perfect, companies operating in the U.S. should incorporate these energy transition scenario projections in their strategic planning initiatives. While there is nuance between industries— some having no choice but to select cleaner combustion fuels for high-heat or energy-intensive industrial processes— many will be faced with evaluating these bridge fuels or pursuing electrification in the short term. According to these latest models, however, the carbon intensity of grid electricity may well be on par with these fuel sources by 2030. Investing in alternative lower-emissions fuels like renewable gas, hydrogen, and methanol may not make sense when electrification is poised to not only be cheaper, but also generate a much larger cut in carbon emissions than before the IRA and IIJA.